EXHIBIT 99.1

Published on November 7, 2025

Exhibit 99.1

P o w er in g H u ma ni t y f r om a M il e U n de r g r o u n d DeepFissi o n . c om T he F as t est P ath t o S c a l e Nu c l e ar P ow er N o v em b e r 5, 2 0 25

L e g a l Di s c l a i m er — F or w a r d - L oo ki n g S ta t e m e nts This p r esentation contains f or w a r d - looking statements within the meaning of the U.S. f ederal securities l a ws, including, among o ther things, statements r ega r ding Deep Fission, In c .’s d e v elopment plans, anticipated p r o je c t timelines, cost o b je c ti v es, comme r cialization strateg y , partnerships, and o ther futu r e matters. F or w a r d - looking statements a r e based on cur r ent e xpe c tations and assum p tions and i n v ol v e risks and uncertainties that could cause a c tual r esults to dif f er materially f r om those e xp r essed or implied. Important fa c tors that could cause such dif f e r ences a r e described under “Risk F a c tors” and “Special N o te Rega r ding F or w a r d - Looking Statements” in Deep Fission’s r egistration statement on F orm S - 1 (as amended f r om time to time) and in o ther filings Deep Fission ma k es with the U.S. Securities and E x change Commission (“SEC”). Deep Fission underta k es no obligation to update or r e vise a n y f or w a r d - looking statements, wh e ther as a r esult of n e w in f ormation, futu r e e v ents, or o therwis e , ex ce p t as r equi r ed b y l a w.

Co r e Idea and Origin Story The Economist Pil o t Rea c tor D e v elopment F o x Business N e t w ork CEO O v ervi e w EnerCom De n v er Con f e r ence 3 Initial Planned Sites W orld Nuclear N e ws 12.5 G W in Pipeline Bloombe rg $30M Financing, Go - Public T ransa c tion Bloombe r g | P ow er T echnology | P r ess Release D eep F is s ion is l ev e r a gi n g th e E arth ’s o w n p h y si c s t o r ed e f i n e the tim e an d c os t o f n u cl ea r p o w er dep l o ym e n t. Cl e an e n e r gy f or the AI e r a.

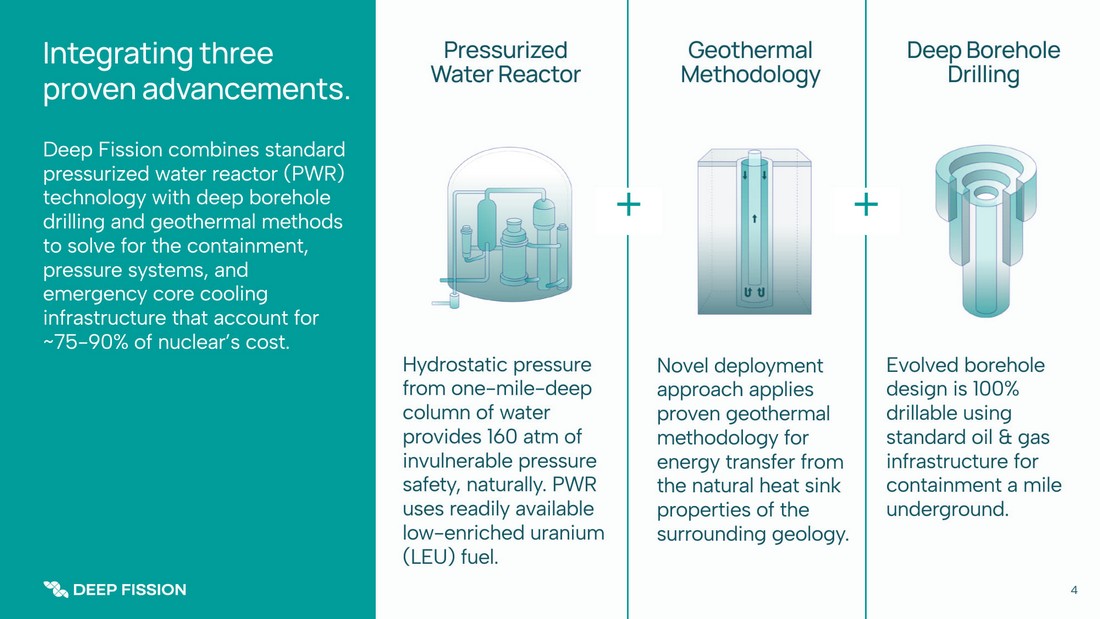

4 I n t e g r at i n g th r ee p r o v e n ad v a n c e m e nts. G e o t her m a l Me tho do l o gy D e e p B o r eho l e D r i l l i ng + + H y d r ostatic p r essu r e f r om one - mile - deep column of w ater p ro vides 160 atm of i n vulnerable p r essu r e sa f e t y , naturall y . PWR uses r eadily a v ailable l o w - enriched uranium (LEU) fuel. N ov el depl o yment app r oach applies p rov en ge o thermal m e thodology f or ene r gy trans f er f r om the natural heat sink p r operties of the sur r ounding geolog y. E v ol v ed bo r ehole design is 100% drillable using standa r d oil & gas infrastru c tu r e f or containment a mile unde r g r ound. P r e s sur i z ed W a t er R e ac t o r Deep Fission combines standa r d p r essurized w ater r ea c tor (PWR) technology with deep bo r ehole drilling and ge o thermal m e thods to sol v e f or the containment, p r essu r e systems, and eme r gen c y co r e cooling infrastru c tu r e that account f or ~75 - 90% of nuclear’s cost.

5 Re g u l a t o r y A d v anta g e: D e e p Fi ss i on se l e c t ed as o n e of 10 c o mp an i es f or the U . S . D e part m e nt of E n e r gy Nu c l e ar R e a c t or P il ot P r o g r a m — A fast - t ra c k in i t i ati v e t o d es ign, b u ild , a nd op e r ate ad v a n ced t est r ea c tor s, wi t h the a m bit io u s go al o f r ea chi ng c rit i ca li ty by J u l y 4, 2026. August 12, 2025 W ASHIN GT ON — The U.S. Department of Ene r gy (DOE) tod a y of f icially kic k ed off P r esident T rump’s Nuclear Rea c tor Pil o t P r ogram, announcing DOE will initially w ork with 11 ad v anced r ea c tor p r o je c ts to m ov e their technologies t ow a r ds depl o yment. DOE will w ork with industry on these 11 p r o je c ts, with the goal to constru c t, operat e , and achi ev e criticality of at least th r ee test r ea c tors using the DOE authorization p r ocess b y July 4, 2026. T od a y’s initial sele c tions r ep r esent an important step t ow a r d st r eamlining nuclear r ea c tor testing and unleashes a n e w path w a y t ow a r d fast - tracking comme r cial licensing a c tivities . “P r esident T rump’s Rea c tor Pil o t P r ogram is a call to a c tion,” sai d Deputy Sec r e tary of Ene r gy James P . Danl y . “These companies aim to all sa f ely achi ev e criticality b y Independence D a y , and DOE will do ev erything w e can to support their ef f orts. ” Seeking DOE authorization p ro vided under the Atomic Ene r gy A c t will help tod a y’s sele c ted companies — Aalo Atomics In c ., Anta r es Nuclear In c ., Atomic Alche m y In c ., Deep Fission In c ., Last Ene r gy In c ., Oklo In c ., Natura Resou r ces L L C , Radiant Industries In c ., T er r estrial Ene r gy In c ., and V alar Atomics In c . — unlock pri v ate funding and p ro vide a fast - trac k ed app r oach to futu r e comme r cial licensing a c tivities.* *U.S. Department of Ene r g y . (2025, August 12). Department of Ene r gy announces initial sele c tions f or n e w r ea c tor pil o t p r ogram. 5

6 Mark P érè s VP E n gi n eeri n g 40+ y ears in Nuclear Engineering M ich ae l B r a s e l COO 30 y ears ac r oss nuclear, f ossil, r en ew able ene r gy A ny a Scud er i Strat e gi c Finan ce 10 y ears e xperience in ene r gy capital mar k e ts Ra ni F r a n o v ich VP R eg ulato ry Aff a irs 30 y ears at NRC K w ad w o Adu t wum N u c l e a r R e a c to r Co r e Desig n E n gi n ee r Holte c , Dominion, X Cel Mark Sch m i t z C F O 40+ y ears global f inance leadershi p , f ormer C F O , It r on, Good y ear, Plug P ow er J a s o n P ot t orf Pri n ci pal I &C Sa f e t y A nal ysis E n gi n eer 25 y ears in comme r cial nuclear ene r gy sa f e ty B r y a n B l a ck VP B u si n ess D ev e lo p m e nt 15 y ears in nuclear and p ow er se c tors E li z a b et h M ull er C E O and Co - F ound e r Co - F ounder, Boa r d Chair & F ormer CE O , Deep Isolation (nuclear w aste disposal) Co - F ounder, Ber k el e y Earth R ich a r d M ull er PhD CT O and Co - F ound e r Co - F ounder, Deep Isolation MacArthur “Genius” 80+ nuclear patents P r o f essor Emeritus , UC Ber k el ey Cultu r e of colle c ti v e dri v e , ecosystems ov er empi r es, and AI - nati v e agilit y. Meet the n e w f a c e of nu c l e a r. Chl oe F r ader VP o f St r at egic Aff a irs 15 y ears in startups, political and f inance se c tors

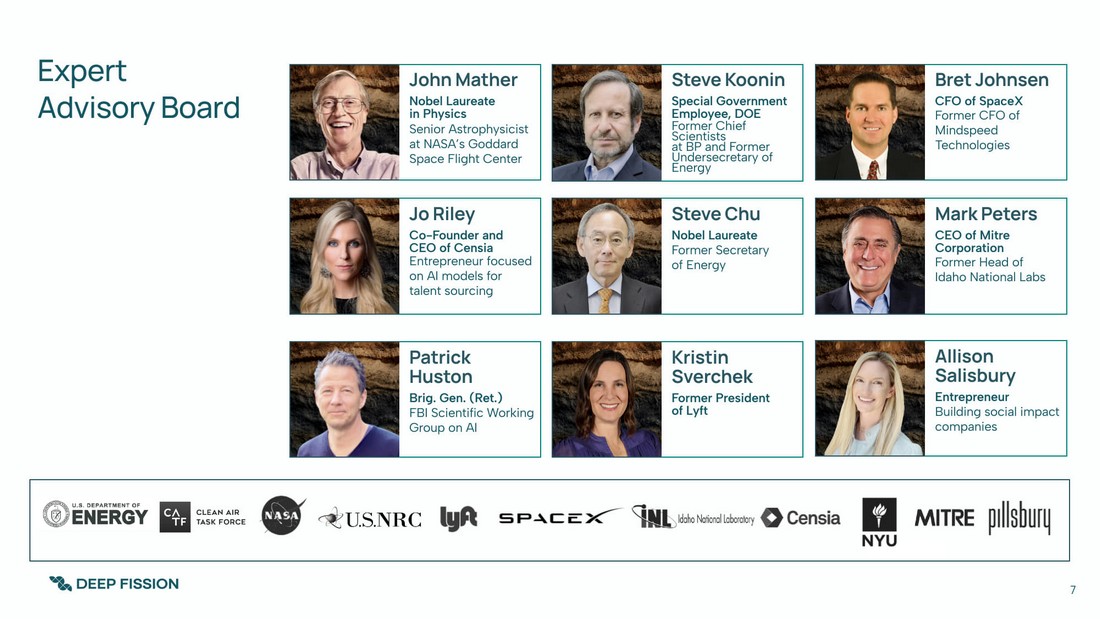

Exp ert A d vi so r y B oa rd S t ev e K oo nin Sp e cial G ov e rnm e nt E m p l o y e e , DOE F ormer Chief Scientists at BP and F ormer Undersec r e tary of Ene r gy P atr i ck Hus t o n Brig. Ge n . (R e t .) FBI Scienti f ic W orking G r oup on AI S t ev e Chu N o be l L au r e at e F ormer Sec r e tary of Ene r gy Kr is t in S v e r ch ek F or m er P r eside n t o f Lyft J o R il e y Co - F ound e r and C E O o f C e n s ia Ent r ep r eneur f ocused on AI models f or talent sou r cing Mark P e t e r s C E O o f M it r e Corporation F ormer Head of Idaho National Labs Allis o n S a lis b u r y E nt r ep r e n e u r Building social impa c t companies J o hn Mat h er N o be l L au r e at e in Ph y sics Senior Ast r ophysicist at NASA’s Godda r d Space Flight Center 7 B r e t Jo hns e n C F O o f Spa ce X F ormer C F O of Mindspeed T echnologies

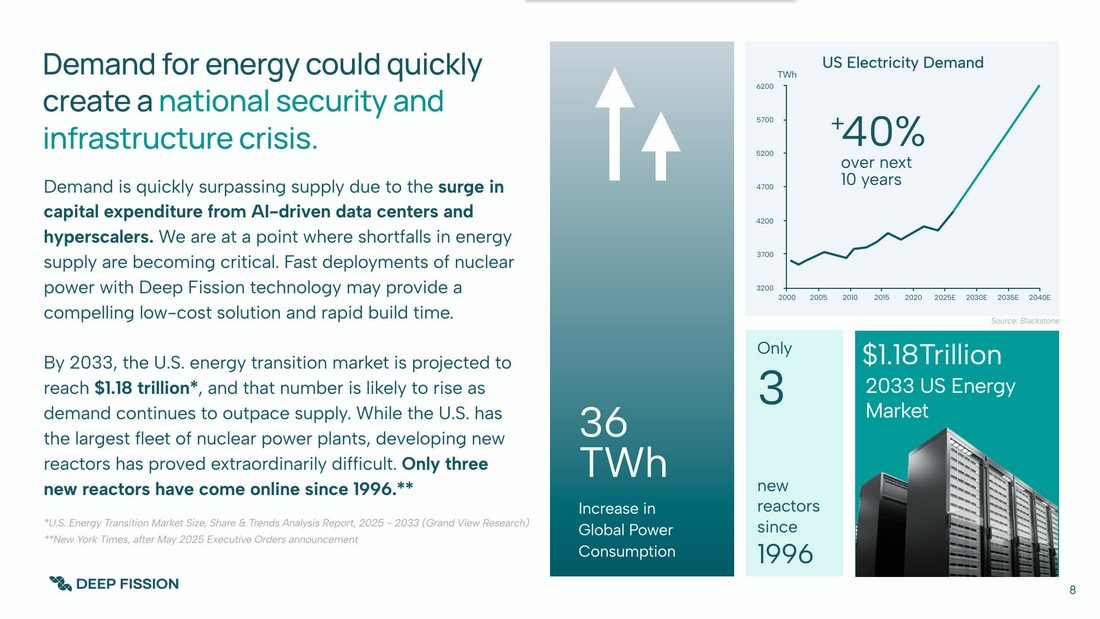

Demand is quickly surpassing supply due to the su r ge in capital e xpenditu r e f r om AI - dri v en data centers and hyperscalers. W e a r e at a point whe r e shortfalls in ene r gy supply a r e becoming critical. F ast depl o yments of nuclear p ow er with Deep Fission technology m a y p ro vide a compelling l o w - cost solution and rapid build tim e . By 2033, the U.S. ene r gy transition mar k e t is p r o je c ted to r each $1.18 trillion * , and that number is li k ely to rise as demand continues to outpace suppl y . While the U.S. has the la r gest f le e t of nuclear p ow er plants, d ev eloping n e w r ea c tors has p rov ed e xtrao r dinarily dif f icult. Only th r ee n e w r ea c tors h a v e come online since 1996.** *U.S. Ene r gy T ransition Mar k e t Siz e , Sha r e & T r ends Analysis Report, 2025 - 2033 (Grand Vi e w Resea r ch) **N e w Y ork T imes, after M a y 2025 E x ecuti v e O r ders announcement 36 TWh Inc r ease in Global P ow er Consum p tion 2033 US Ene r gy Mar k et D e m a n d f or e n e r gy c ou l d qu ickly c re a t e a nat i ona l se c ur i t y a n d i nf r astru c tu r e c r i s i s. Onl y $1.18 T rillion 3 n e w r ea c tors since 1 9 96 8 3200 3700 4200 4700 5200 5700 6200 2000 2005 2010 2015 2020 2025E 2030E 2035E 2040E 40% ov er n e xt 10 y ears + US Ele c t ri c i t y Dema nd T Wh Sou r ce: Blackstone

T raditional/Surface L ev el Rea c tors C r ed ibili t y , c o st & c o mpl e xi t y a r e b arr i e r s — W e a r e in a r a c e agains t t i m e. C r edibl e , sa f e solutions ta k e decades to build, m a ximize pushback, and often amplify costs to the point of cancellation. N e xt - Gen SMRs Small modular r ea c tors a r e hinde r ed b y their ability to p r oduce cost - ef f e c ti v e ele c tricity in the near term. N ov el Rea c tor Startups N e w solutions pose high risk with unp rov en upside — iterati v e , untested tech as opposed to wholesale b r eakth r ough. D e e p Fi ss i on i s des ig n ed f or r apid d e pl o y m e nt, built with sta n da r d t e c h n o l o g y , a n d e n gi n ee r ed f or e c o n o mic t r ans f or m at i on. The DOE has decla r ed a nuclear fast - track with a ta r g e t to achi ev e criticality of at least th r ee test r ea c tors b y July 4, 2026. Deep Fission beli ev es it has a plan and path to be one of those th r e e. 9

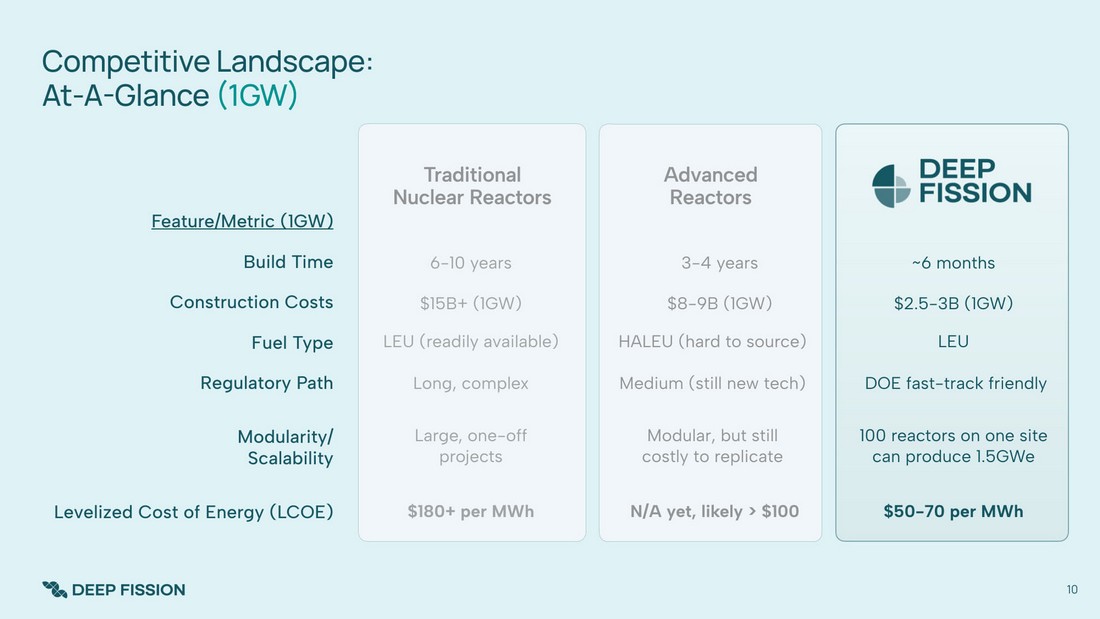

C o mp et i t i v e L a n ds c a p e: A t - A - Gl a n c e (1 G W) 10 6 - 10 y ears 3 - 4 y ears ~6 months $15B+ (1 G W) $8 - 9B (1 G W) $2.5 - 3B (1 G W) LEU ( r eadily a v ailable) HALEU (ha r d to sou r ce) LEU Long, compl e x Medium (still n e w tech) DOE fast - track friendly La r g e , one - off p r o je c ts Modular, but still costly to r eplicate 100 r ea c tors on one site can p r oduce 1.5 G We $180+ per MWh N/A y e t, li k ely > $100 $50 - 70 per MWh Build T ime Constru c tion Costs Fuel T ype Regulatory P ath F eatu r e/M e tric (1 G W) T raditional Nuclear Rea c tors Ad v anced Rea c tors Modularity/ Scalability L e v elized Cost of Ene r gy ( L COE)

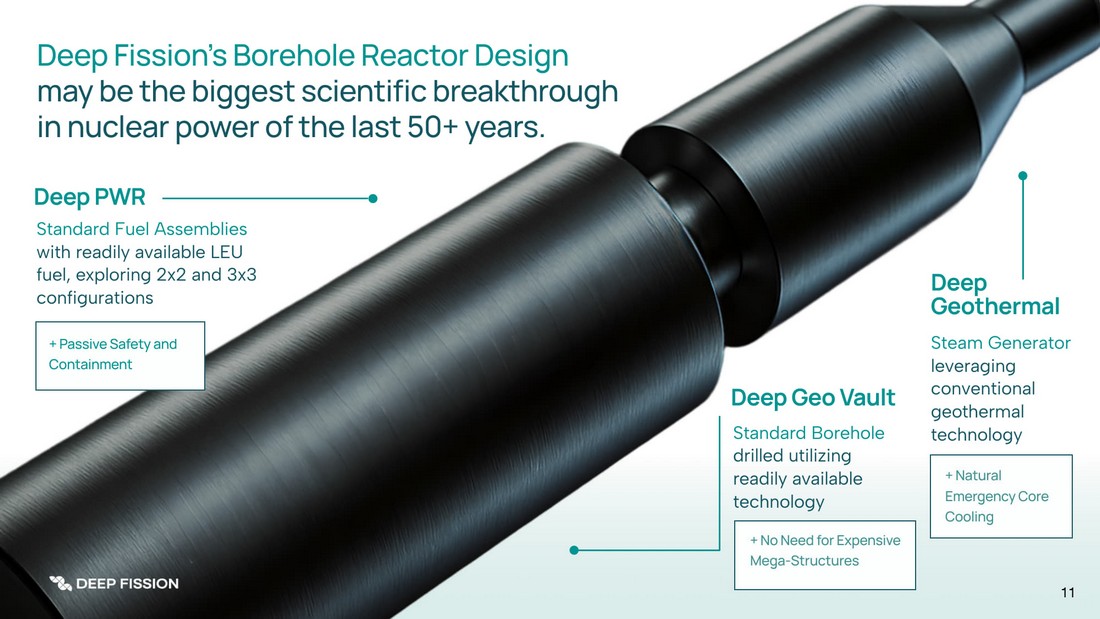

11 Standa r d Fuel Assemblies with r eadily a v ailable LEU fuel, e xploring 2x2 and 3x3 con f igurations D e e p PWR D e e p Geo V a ult Steam Generator l ev eraging co nv entional ge o thermal technology D e e p Ge ot h er m al Standa r d Bo r ehole drilled utilizing r eadily a v ailable technology D e e p Fi ss i o n ’ s B o r eho l e R e a c t or D es ig n m a y b e the bigg est s c i e nt i f ic b re a k th r ou g h i n nu c l e ar p o w er of the l ast 5 0+ y e a r s. + P a s s i v e S a f e t y a n d C o nt a i n m e nt + N o N ee d f or Exp e n s i v e Me g a - S tru c tu r es + N a t u r a l E m e r g e n c y C o r e C oo li ng

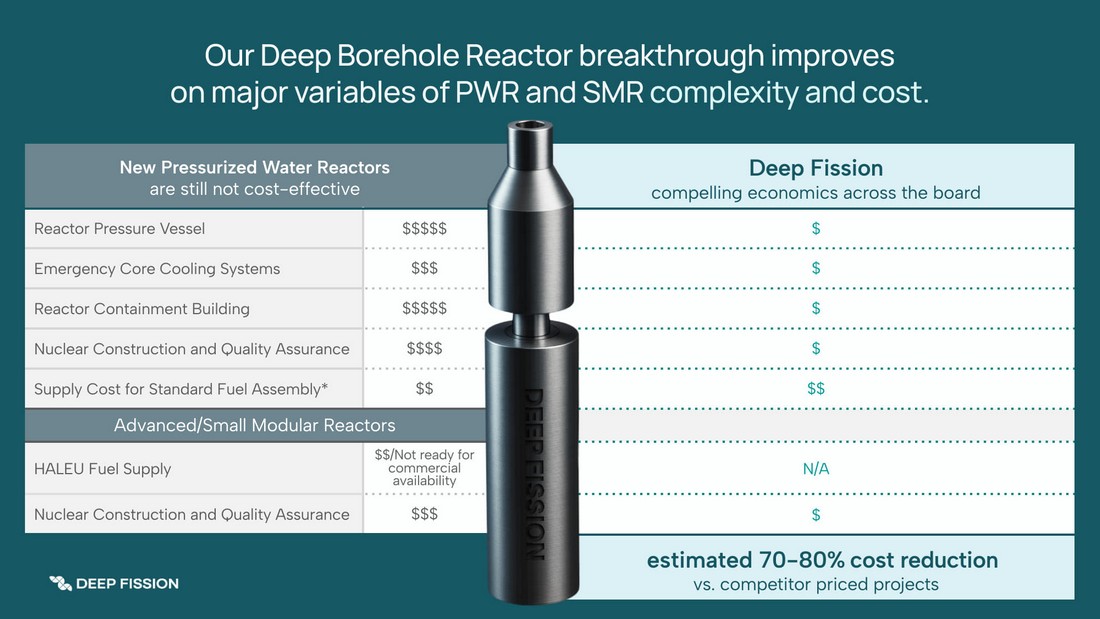

N e w P r ess u ri z e d W at er R e a c to rs a r e still n o t cost - ef f e c ti ve Deep F issi on compelling economics ac r oss the boa rd Rea c tor P r essu r e V esse l $$$$ $ $ Eme r gen c y Co r e Cooling System s $$ $ $ Rea c tor Containment Buildin g $$$$ $ $ Nuclear Constru c tion and Quality Assuranc e $$$ $ $ Supply Cost f or Standa r d Fuel Assembly * $ $ $$ Ad v anced/Small Modular Rea c tors HALEU Fuel Supply $$/N o t r eady f or comme r cial a v ailability N/A Nuclear Constru c tion and Quality Assuranc e $$ $ $ estimated 70 - 80 % c o s t r ed u c t i o n vs. comp e titor priced p r o je c ts O ur D e e p B o r eho l e R e a c t or b re a k th r ou g h imp r o v es on m a j or v ar i a bl es of P W R a n d S M R c ompl e xi t y a n d c o st.

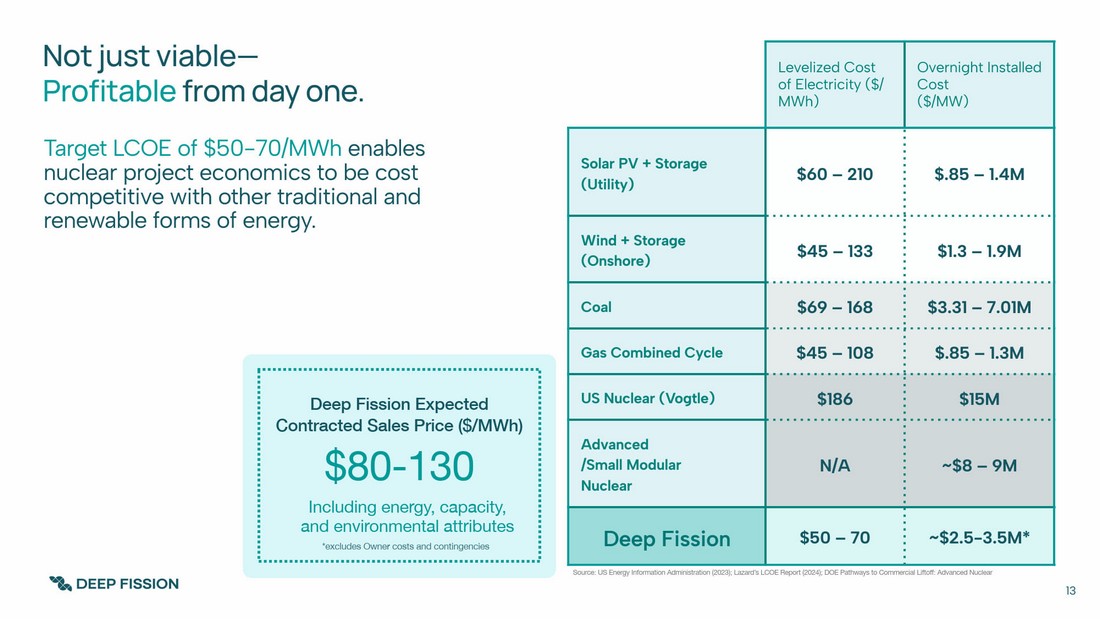

Not j ust vi a bl e — P r o f i ta bl e f r o m d a y o n e. Sou r ce: US Ene r gy Information Administration (2023); Laza r d ’ s LCOE Report (2024); DOE Pathways to Comme r cial Lifto f f: Advanced Nuclear Including ene r g y , capacit y , and envi r onmental attributes Deep Fission Expected Contracted Sales Price ($/MWh) $80 - 1 30 L ev elized Cost of Ele c tricity ($/ MWh) O v ernight Installed Cost ($/MW) Solar PV + Storage (Utility ) $60 – 21 0 $.85 – 1.4M Wind + Storage (Onsho r e ) $45 – 13 3 $1.3 – 1.9M Coa l $69 – 16 8 $3.31 – 7.01M Gas Combined C y cl e $45 – 10 8 $.85 – 1.3M US Nuclear ( V ogtle ) $18 6 $15M Ad v anced /Small Modular Nuclear N/ A ~$8 – 9M Deep F issi o n $50 – 7 0 ~$2.5 - 3.5M* 13 T a r g e t L CO E of $5 0 - 70/MW h e n a b l e s nu c l e a r p r o j e c t econom i cs t o b e c o s t c om p e t i t i v e with o th e r trad i t i o na l a n d r e n e w a ble f o rms o f ene r g y.

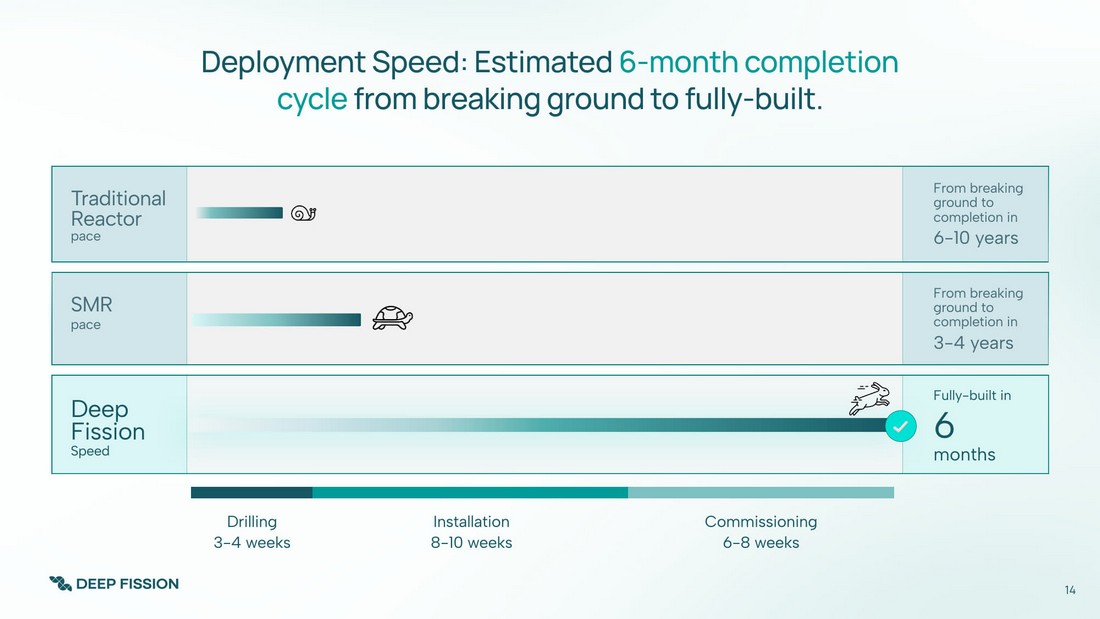

T raditional Rea c tor pace F r om b r eaking g r ound to compl e tion in 6 - 10 y ears SMR pace F r om b r eaking g r ound to compl e tion in 3 - 4 y ears Deep Fission Speed Fully - built in 6 months Drilling 3 - 4 w eeks Installation 8 - 10 w eeks D e pl o y m e nt Sp eed: E st im a t e d 6 - m onth c o mpl et i on cy c l e f r o m b re a ki n g g r ou n d t o fu lly - b u il t. Commissioning 6 - 8 w eeks 14

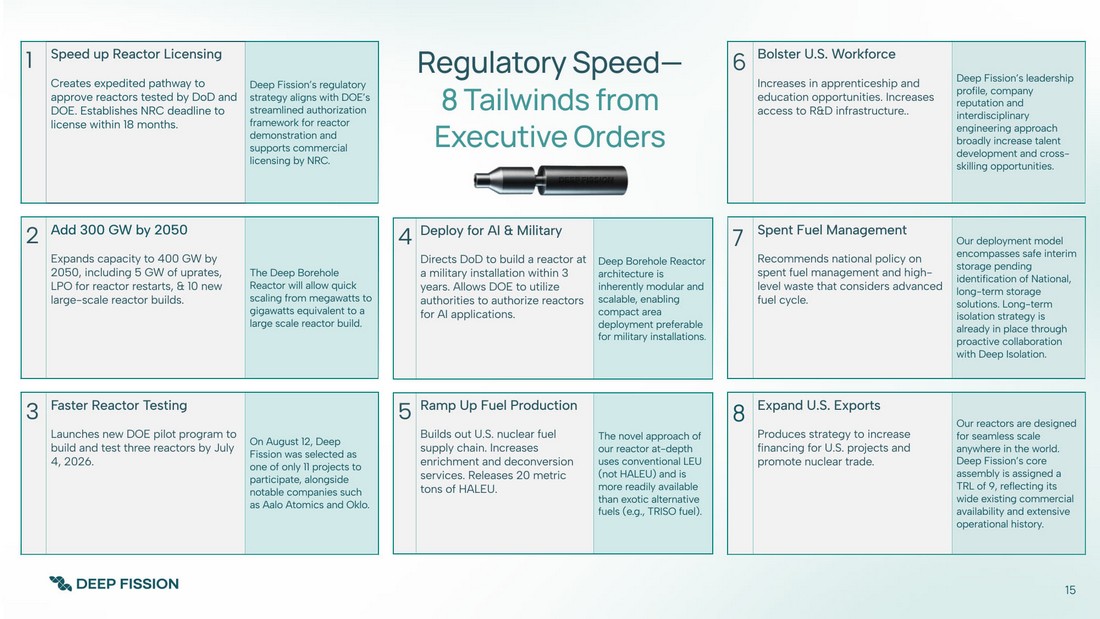

Re g u l a t o r y Sp eed — 8 T a ilwi n ds f r o m E x e c ut i v e O r de rs 1 Speed up Rea c tor Li c ensin g C r e a te s e xp e d i t e d pa th w a y to a pp ro v e r ea c to r s te ste d b y DoD an d DO E. Es t abl is he s NRC d ead l i n e to lic e nse w i t h i n 1 8 m o n th s. Deep Fission’s r egulatory strategy aligns with DOE’s st r eamlined authorization fram ew ork f or r ea c tor demonstration and supports comme r cial licensing b y NR C. 2 A dd 300 G W b y 2 05 0 Ex p a n d s c a p ac i t y t o 40 0 G W b y 20 5 0 , in c l u di n g 5 G W o f u p r a t es, LPO f o r r ea c t o r r e st ar ts , & 10 n e w l a r g e - s cal e r e a c t or bui l d s. The Deep Bo r ehole Rea c tor will all o w quick scaling f r om meg a w atts to gig a w atts equi v alent to a la r ge scale r ea c tor build. 3 F as t er Rea c t or T es t ing La u n ch e s n e w D OE p i l o t p r o g r a m t o b u il d a n d te s t t h r e e r e a c to r s b y Jul y 4 , 2 0 26. On August 12, Deep Fission w as sele c ted as one of only 11 p r o je c ts to participat e , alongside n o table companies such as Aalo Atomics and Okl o. 6 B o ls te r U . S . W o r k f o r ce I n c r ease s i n a p p r e n t i c e sh i p a n d ed u ca ti on op p o r tu n i ti e s. I nc r ea s es a c c e s s t o R & D i n f r a st ru c tu r e .. Deep Fission’s leadership p r o f il e , compa n y r eputation and inte r disciplinary engineering app r oach b r oadly inc r ease talent d ev elopment and c r oss - skilling opportunities. 7 Spent Fuel Managemen t R ec o mmen d s n at io n a l p ol i c y o n sp ent fu el ma n ag e m en t an d hi g h - l ev e l w as t e t ha t c o n si d er s a d v a n ce d fue l cy c l e. Our depl o yment model encompasses sa f e interim storage pending identi f ication of National, long - term storage solutions. Long - term isolation strategy is al r eady in place th r ough p r oa c ti v e collaboration with Deep Isolation. 8 Expand U.S. Expor t s P r od uce s str a t e g y to i nc r ea se f i n a nci ng f or U . S. p r o j e c t s a n d p r o m o te n u cl ea r tr a d e. Our r ea c tors a r e designed f or seamless scale a n ywhe r e in the w orld. Deep Fission’s co r e assembly is assigned a TRL of 9, r e f le c ting its wide e xisting comme r cial a v ailability and e xtensi v e operational histor y . 4 Depl o y f or AI & Militar y Di r e c t s D oD to b u il d a r e a c tor a t a m i l i tar y i ns t al l a tio n wi th i n 3 y e ars . A ll o w s DO E t o u t il i z e a uth o r i ti e s to au th ori z e r e a c t o r s f or A I a pp li cat i o n s. Deep Bo r ehole Rea c tor a r chite c tu r e is inhe r ently modular and scalabl e , enabling compa c t a r ea depl o yment p r e f erable f or military installation s . 5 R a mp Up F uel P r odu c t i o n B u i ld s o u t U .S . n uc le ar fue l su p p l y ch a in . In c r ea se s en r i ch ment and de c o n v er si o n s e rvi c es . Re l ea ses 20 m e t r ic to n s o f H AL EU. The n ov el app r oach of our r ea c tor at - de p th uses co nv entional LEU (n o t HALEU) and is mo r e r eadily a v ailable than exo tic alternati v e fuels ( e. g., TRISO fuel). 15

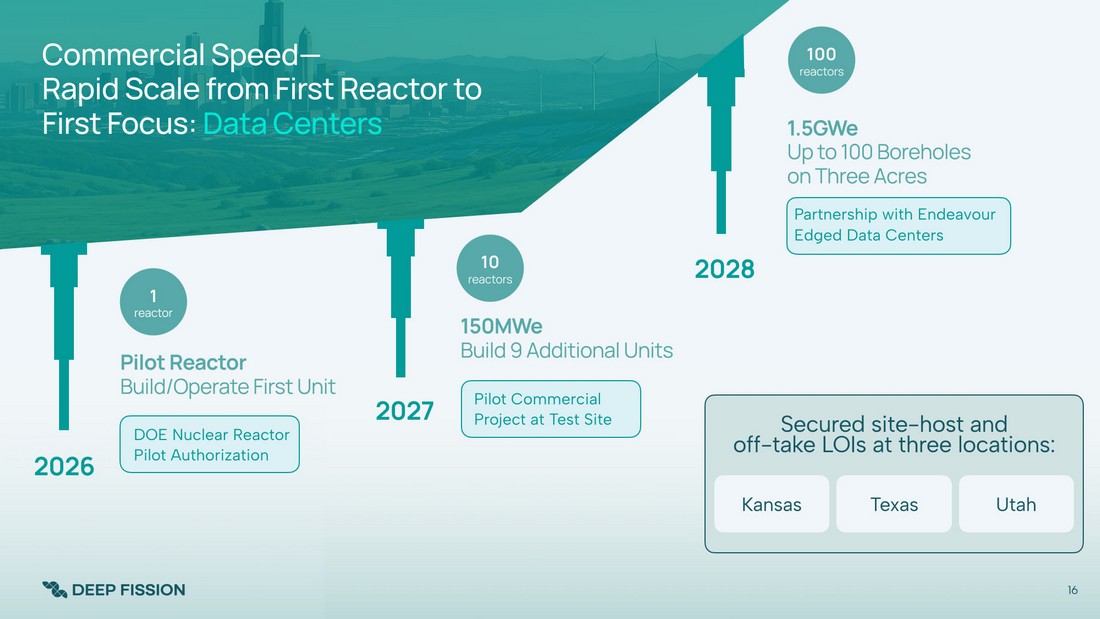

100 C o m m e r c i a l Sp eed — re ac t o rs Ra pi d S c a l e f r o m Fi r st R e a c t or t o Fi r st F o c us : D ata C e n t e r s 1 . 5 G W e Up t o 100 B o r e h ole s o n T h r ee Ac r es 10 re ac t o rs 16 150M W e Bu ild 9 Additio n al Un its S ecu r e d site - host a nd o f f - ta k e L OI s a t t h r e e loca t i o ns: K ansa s T e xa s Utah 2 0 27 2 0 28 DOE Nuclear Rea c tor 2 0 2 6 Pil o t Authorization Pil ot R e a c t or Bu ild/O p e r a t e Fi r s t Un it 1 re ac t or Pil o t Comme r cial P r o je c t at T est Site P artnership with Ende a v our Edged Data Centers

Deep Fission is partne r ed with Ende a v our, a sustainable data center + infrastru c tu r e compa n y , to co - d ev elop 2 G W of nuclear ene r g y , supporting sales to major cloud p ro viders. This partnership c r eates a di r e c t comme r cial path w a y f or Deep Fission r ea c tors in one of the fastest - g ro wing ele c tricity demand se c tors, l ev eraging its unique ability to deli v er r eliabl e , ze r o - carbon baseload p ow er at scal e. L a n d m ar k P art n e r sh i p W it h E n d e a v our 17 Full Ende a v our P ort f olio: W orld Nuclear News

A cc e l e r a t e d I n n o v at i on — D e e p Fi ss i on i s a n e w c lass of inf r astructu r e . Deep Geologic L ev erage DBR Canister Design Deep Casing & Containment Rapid Install, O&M Deep Sa f e ty & Security • Shielding • Containment • Security • P r essurization • Rock moderation • Choice of de p th • Butter f ly • Ladybug • Lune d o wncorner • Lune f ill • Rock moderation • Choice of de p th • Steam generator • Cigar burn • L a y out • Centralizer • Cement • Instrument access • Additi v es • Coiled tubing • Casing f ill • P r e - fab • Re - f ill • AI • Load f oll ow • Geologic • Steam cooling • ECCS • Air ex clusion Co r e Conce p t Stack Deep Bo r ehole Nuclear Rea c to r Storage & Deep Steam 24 P ending Applications; 1 US Application All ow ed 40+ Unique Inn ov ations and N ov el Conce p ts IP p r o cess is e xped i ted vs . c om p e t it or s , a nd p o r t f o lio of 7 pate n t f am i li e s c r eat es lo ng - t e r m IP mo a t a nd l ic e nsi n g p o t ent i a l . 18

P r o pr i et a r y an d C on f i d e nt i al | | 19 N ov e l D e e p B o r ehol e R e a c tor i n t e gra te s n uc le a r e n e r g y with p r o v e n o i l a nd gas te c h n ologi es , enabl i ng r a pid, r e pea t a b l e , h i gh - v ol u m e dep l o y me n t . This s t rate g y s i m p li f i es th e s a f e t y c as e , r e d u c es e m e r ge n c y p lann i ng z ones, a n d en a bl e s r e a c t o r si t ing i n p re v iou s l y i n ac c ess i bl e ma r k e t s. Fir s t major b r e a k th r ough in th e nu c l e a r i ndu s t ry i n 5 0 y e a rs E s t im a t e d 80 % c o st - s a vin g s o v er co mp e tit o r p r o je c t e d co sts du e to d r as t i c a ll y - r ed uce d c o n s t r u c tio n budg e t s a n d ti m e l i n e s . P r o je c t f in a n c ing i nclud e s a te c h n ology l i c e ns in g f e e that c ov e rs t h e fu ll co st o f t he f irst c omm e r c i a l p r o j e c t i n 202 6 a f t e r r e ce ivi n g a n e xp e d it ed l i ce n s e f r om th e NR C . High RO I is unmat ched f o r a f ir s t - o f - a - k ind p r o je ct De e p F i s s i on ’ s r e a c t o r p i l o t p r ogra m s tr at e g y a l ig n s pe r f e c tly w i th P r esi d en t T r u mp ’ s na tion a l s e c ur i t y an d e n e r gy goals to e n s u r e U .S. domi n a n ce g l oba l l y . Furt he r , th e u s e of c o mme r c i a l l y p ro v e n te c h n ologi es als o f a c i li t a t es r egulatory a c c e p ta n ce a n d r ed u c e s the d ev el o p m e n t b u r d en asso cia t ed w it h n o v e l compo n e n t l ice n s i ng . I n v es tm e nt i s a cce l e rat e d b y sig n i f ic ant po l i c y ta i l wi n ds P ro vi s i on al p a tent s on using n a t ural p r o p e r ti es o f the d e ep su b - surfac e t o r educ e t h e c o st o f n u cl e ar p ow er c r e at e s i g n i f i can t I P l i cens i n g p o te n ti a l. L O I ne g o t i a t i o ns unders c o r e te c hnologi c al r e a din e ss a nd c om p ellin g economi c s e v e n f o r e st ab li sh e d pl a y ers in t he i n d ust r y , on top o f r e a c t or sys te m sal e s, l i f e c y cl e se rv i ces , and Bu i ld - Own - O pe r a te r ev e nue s t r e a ms. P lat f o r m r ev e nu e mo de l wi t h t ech t r an s f er opportuniti es 1 2 3 4 T h i s m a y b e the m o st imp ortant i n v est m e nt of our li f et i m e — Emp ow ering a winning nuclear technology is k e y to leadership in the age of AI. 8 m o n t h s t o J u ly 4 , 2026 19

S cala b le B r oad - range mar k e t serviceability f r om 15 M W e to 1.5 G We. R e ad ine ss DOE pil o t p r ogram sele c tion o b tained. Pil o t facility b y July 2026. L OIs f r om f our p r ospe c ti v e sites. A f f o r da b le T a r g e t $50 - 70 per MWh f or continuous suppl y. S p eed Estimated 6 months f r om b r eaking g r ound to p r odu c tion. P r ov en N ov el combination of p rov en nuclear and ge o thermal technologies. S a f e ty One mile unde r g r ound with natural containment and p r essu r e. S u mm a r y I n v est m e nt T hes i s 20

P o w e r i n g H u m a n i t y f r o m a M i l e U n de r g r ou n d F o r i n v es to r inquiries, c o n t a c t : Bob Prag IR@deep f ission . com (858) 794 - 9500 F o r media inquiries, c o n t a c t : Chloe Frader VP Strategic Affairs chlo e .frader@deep f ission . com T he F as t est P ath t o S c a l e Nu c l e ar P ow er